Statement outlining results, risks and significant changes in operations, personnel and program

A) Introduction

Statistics Canada’s mandate

Statistics Canada is a member of the Industry Portfolio.

Statistics Canada’s role is to ensure that Canadians have access to a trusted source of statistics on Canada that meet their highest priority needs.

The Agency’s mandate derives primarily from the Statistics Act. The act requires that Statistics Canada collect, compile, analyze and publish statistical information on the economic, social and general conditions of the country and its people. It also requires that Statistics Canada conduct a census of population and a census of agriculture every fifth year, and protect the confidentiality of the information with which it is entrusted.

Statistics Canada is also mandated to coordinate and lead the national statistical system. The Agency is considered a leader among statistical agencies around the world in coordinating statistical activities to reduce duplication and reporting burden.

Further information on Statistics Canada’s mandate, roles, responsibilities and programs can be found in the 2012-2013 Main Estimates and in the Statistics Canada 2012-2013 Report on Plans and Priorities.

The quarterly financial report

Statistics Canada has the authority to collect and spend revenue from other government departments and agencies, as well as external clients, for statistical services and products.

Basis of presentation

This quarterly report has been prepared by management using an expenditure basis of accounting. The accompanying Statement of Authorities includes the Agency’s spending authorities granted by Parliament and those used by the Agency consistent with the Main Estimates for the 2012-2013 fiscal year. This quarterly report has been prepared using a special purpose financial reporting framework designed to meet financial information needs with respect to the use of spending authorities.

The authority of Parliament is required before moneys can be spent by the Government. Approvals are given in the form of annually approved limits through appropriation acts or through legislation in the form of statutory spending authority for specific purposes.

As part of the Parliamentary business of supply, the Main Estimates must be tabled in Parliament on or before March 1 preceding the new fiscal year. Budget 2012 was tabled in Parliament on March 29, after the tabling of the Main Estimates on February 28, 2012. As a result the measures announced in the Budget 2012 could not be reflected in the 2012-13 Main Estimates.

In fiscal year 2012-2013, frozen allotments will be established by Treasury Board authority in departmental votes to prohibit the spending of funds already identified as savings measures in Budget 2012. In future years, the changes to departmental authorities will be implemented through the Annual Reference Level Update, as approved by Treasury Board, and reflected in the subsequent Main Estimates tabled in Parliament.

The Agency uses the full accrual method of accounting to prepare and present its annual departmental financial statements that are part of the departmental performance reporting process. However, the spending authorities voted by Parliament remain on an expenditure basis.

B) Highlights of fiscal quarter and fiscal year-to-date results

This section highlights the significant items that contributed to the net decrease in resources available for the year and actual expenditures for the quarter ended September 30.

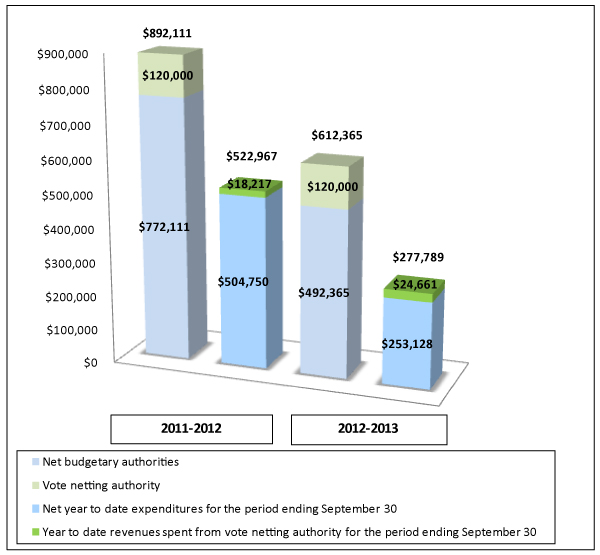

Chart 1: Comparison of gross budgetary authorities and expenditures as of September 30, 2011 and September 30, 2012, in thousands of dollars

Chart 1 outlines the gross budgetary authorities, which represent the resources available for use for the year as of September 30.

Significant changes to authorities

During the second quarter, Statistics Canada authorities increased $37.7 million. This is related to the carry-forward of funds from fiscal year 2011-2012 to fiscal year 2012-2013.

Total authorities available for the year have decreased $279.7 million, or 31.4% from the previous year, from $892.1 million to $612.4 million (Chart 1). This net decrease is mostly due to the completion of collection activities of the 2011 Census of Population and National Household Survey ($248.5 million) and the 2011 Census of Agriculture ($13.3 million). Fiscal year 2011-2012 was the peak year for census-related activities.

The primary census-related activities for 2012-2013 are

- conducting evaluation studies;

- continuing data certification and processing activities for the National Household Survey;

- disseminating major data releases, data quality studies, and evaluation of results for the Census of Population and the Census of Agriculture; and

- linking the 2011 Census of Agriculture and the 2011 National Household Survey to produce a database of socioeconomic information on farm operators and their families.

The transfer of funds to Shared Services Canada also resulted in a funding decrease of $36.2 million. Funds were transferred to Shared Services Canada to pool existing resources from across the government to consolidate and transform IT infrastructure for the Government of Canada.

In addition to the appropriations allocated to the Agency through the Main Estimates, Statistics Canada also has vote net authority within Vote 105, which entitles the Agency to spend revenues collected from other government departments, agencies and external clients for providing statistical services. Vote netting authority is stable for 2011 2012 and 2012-2013 at $120 million.

Significant changes to expenditures

Total expenditures recorded for the second quarter, ending September 30, 2012, decreased $100.2 million, or 40.4%, from the same quarter of the previous year, from $248.1 million to $147.9 million, according to Table A: Departmental budgetary expenditures by Standard Object.

Most of the decrease in spending is due to the completion of important census-related activities, such as data collection and capturing, which entails the majority of census expenditures. Also, Statistics Canada has spent approximately 45% of its authorities by the end of the second quarter, compared with 59% in the previous year.

Table A: Departmental expenditures by Standard Object (unaudited)

| Departmental Expenditures by Standard Object |

Year-to-year variation, Q2 2011-12 to Q2 2012-13 |

Cumulative year-to-date variation |

|---|

| 000$ |

% |

000$ |

% |

|---|

| (01) Personnel |

-25,642 |

-15.7% |

-54,364 |

-17.3 % |

| (02) Transportation and communications |

-7,022 |

-70.6% |

-33,495 |

-85.2% |

| (03) Information |

-2,980 |

-96.2% |

-8,904 |

-97.9% |

| (04) Professional and special services |

-58,612 |

-95.2% |

-140,123 |

-96.9% |

| (05) Rentals |

-1,520 |

-30.7% |

- 419 |

-6.8% |

| (06) Repair and maintenance |

-2,043 |

-94.8% |

-5,043 |

-97.4% |

| (07) Utilities, materials and supplies |

- 727 |

-71.0% |

- 805 |

-52.1% |

| (08) Acquisition of land, building and works |

0 |

0.0% |

0 |

0.0% |

| (09) Acquisition of machinery and equipment |

-1,550 |

-78.3% |

-1,929 |

-78.3% |

| (10) Transfer payments |

- 134 |

134.0% |

- 134 |

134.0% |

| (12) Other subsidies and payments |

6 |

145.2% |

38 |

230.0% |

| Total gross budgetary expenditures |

-100,224 |

-40.4% |

-245,178 |

-46.9% |

| Less Revenues netted against expenditures: |

|---|

| Revenues |

8,564 |

77.6% |

6,444 |

35.4% |

| Total net budgetary expenditures |

-108,788 |

-45.9% |

-251,622 |

-49.9% |

| Note: For variances of more than $1 million, an explanation is provided. |

01) Personnel: Additional public servants were hired to conduct census-related activities in 2011-2012. The decrease in costs in 2012-2013 is caused by the completion of collection activities, which entails the majority of census expenditures. In addition, the transfer of employees to Shared Services Canada and the impact of cost-containment reductions also contributed to the overall decrease in salary costs. These decreases offset some of the non-recurring costs that have been disbursed in direct relation to the Workforce Adjustment Directive.

02) Transportation and Communication: Additional costs in postage and transportation were incurred in 2011-2012 for census-related activities such as the delivery and return of census questionnaires. The completion of these activities explains the reduction in costs in 2012-2013. The transfer of telecommunication operations to Shared Services Canada also resulted in a cost decrease.

03) Information: In 2011-2012, the census communications program was implemented to support census collection activities, resulting in advertising and printing costs for the Agency. The decrease in costs in 2012-2013 is the result of the completion of this activity.

04) Professional and Special Services: In 2011-2012, approximately 35,000 field staff were recruited and trained to follow up with non-response. The field-collection activities in 2011 also included the pay for census enumerators and advances. The completion of collection activities explains the reduction in costs in 2012-2013.

05) Rentals: A change in the Government-wide Chart of Accounts now requires “Software licenses/maintenance” expenditures to be reported under Standard Object 05 instead of Standard Object 06 — Repairs and maintenance. This change resulted in an increase of expenditures in Standard Object 05. However, this increase is offset by costs incurred to rent building space in 2011-2012 for census collection activities in remote areas. The decreased costs in 2012-2013 are the result of the completion of this activity.

06) Repairs and Maintenance: A change in the Government-wide Chart of Accounts now requires expenditure type “Software licenses/maintenance” to be reported under Standard Object 05 – Rentals instead of Standard Object 06. This change in the Chart of Accounts, combined with Shared Services Canada now taking responsibility for a portion of these expenditures, resulted in the decreased expenditures in Standard Object 06. Furthermore, additional software-maintenance costs to support data collection, processing and dissemination systems were incurred in 2011-2012 for census-related activities. This also contributed to the decrease in 2012-2013; these activities are now complete.

09) Acquisition of machinery and equipment: The decrease is because Shared Services Canada assumed responsibility for purchasing informatics equipment, which falls under Standard Object 09.

The increase in Revenues is primarily because of funds that Statistics Canada receives under a census cost-sharing agreement with another government department; in 2012-2013, those funds were received six months later than they were in 2011-2012.

C) Risks and uncertainties

The pressures created by cumulative budgetary reductions will make 2012-2013 a challenging year for Statistics Canada—the challenge being to remain within appropriations while delivering the core program. Statistics Canada plans to meet these challenges through the following actions and mitigation strategies:

- governance around financial forecasting practices was increased to ensure the Agency remains within its appropriations;

- the level of approval for signing authority on non-salary expenditures has been reviewed, and a temporary overlay on top of the Delegation of Financial Signing Authority is in use to prioritize non-salary spending;

- monthly project dashboards are in place across the Agency to monitor project issues, risks and alignment with approved budgets; and

- as the workforce is reduced, reorganization and reprioritization of work and teams will occur and knowledge will be transferred.

D) Significant changes to operations, personnel and programs

2011 Census of Population and the National Household Survey

In 2012-2013, Statistics Canada is continuing to disseminate its remaining major census data releases, data quality studies, and evaluation of the National Household Survey results. Census of Population releases take place in May, September and October 2012. Data certification and processing activities for the National Household Survey are also progressing as planned, and releases are scheduled from May to August 2013. The main release of the 2011 Census of Agriculture took place on May 10, 2012. More Census of Agriculture products are to be released beginning in September 2012. Data quality studies for the 2011 Census and the National Household Survey will continue through 2012-13.

This contrasts with last year, when the program focused on collection operations and processing returns for the 2011 Census of Population and National Household Survey.

Shared Services Canada

On August 4, 2011, the Government of Canada announced measures to streamline and identify savings in information technology through Shared Services Canada. Resources associated with email delivery and with data centre and network services are being transferred to this new entity. Statistics Canada is one of 44 departments and agencies selected for this new initiative. Statistics Canada transferred 178 positions.

Pursuant to s. 31.1 of the Financial Administration Act and Order-in-Council P.C. 2011-1297 effective November 15, 2011, $36.2 million annually is deemed to have been appropriated to Shared Services Canada on an on-going basis starting in fiscal year 2012-2013, resulting in a reduction for the same amount from Statistics Canada, Vote 105.

E) Budget 2012 implementation

This section provides an overview of the savings measures announced in Budget 2012 that will be implemented in order to refocus government and programs; make it easier for Canadians and business to deal with their government; and, modernize and reduce the back office.

Statistics Canada’s savings target as announced in Budget 2012 Economic Action Plan is $33.9 million by 2014-2015. This reduction will be implemented progressively, beginning with $8.3 million on April 1, 2012, rising to $18.3 million on April 1, 2013, in order to achieve the full reduction by April 1, 2014. In order to meet this target, Statistics Canada has focused resources where they are most needed.

The savings incurred through these program adjustments represent moderate reductions in the production of statistics to support development, administration and evaluation of policy, while continuing to meet the public’s highest priority needs. In some cases, the information will continue to be available in a different format. A full list of program adjustments is available online.

Cost-recovery activities

Statistics Canada is also providing statistical services and products to federal departments and agencies on a cost-recovery basis. Reductions being made in other departments may have a further impact on Statistics Canada.

Workforce Adjustment

A human resources management framework was developed to manage the required adjustments to the Agency’s workforce, which will be further guided by the provisions of the relevant collective agreements, the Workforce Adjustment Directive and the Career Transition Plan for Executives. Statistics Canada is committed to proceeding with these adjustments in a manner that is respectful, fair and transparent at all times.

Approval by senior officials

The original version was signed by

Wayne Smith, Chief Statistician

Michel Cloutier, Chief Financial Officer

Statement of authorities (unaudited)

Departmental budgetary expenditures by Standard Object (unaudited)